Trump’s Tariff Bombshell: 5 Key Takeaways from “Liberation Day

Here is the rewritten article, meeting all the specified requirements:

Equity Markets Reel from Shocking Tariff Announcement

Yesterday marked a pivotal moment in global trade policy as President Trump declared it "Liberation Day" in the midst of a drastic shift towards universal tariffs on imports into the United States. The president’s declaration was met with widespread disappointment, particularly among those expecting the news to be relatively painless. Instead, investors were left grappling with the potential implications of the new trade policies on their portfolios and the broader economy.

The market’s immediate reaction was intense, with a sharp sell-off in global equity markets as investors assessed the potential impact of the tariffs on growth and earnings. The magnitude of the announcement far exceeded expectations, with some analysts suggesting that the tariff rate could jump to 20% or even higher in certain sectors. This is particularly concerning given the historical precedent set by the Smoot-Hawley Act of 1930, which saw the U.S. average tariff rate peak at 20%. Market sentiment took a significant hit, mirroring concerns about recession and lower growth estimates.

Five Key Tariff Takeaways from "Liberation Day"

-

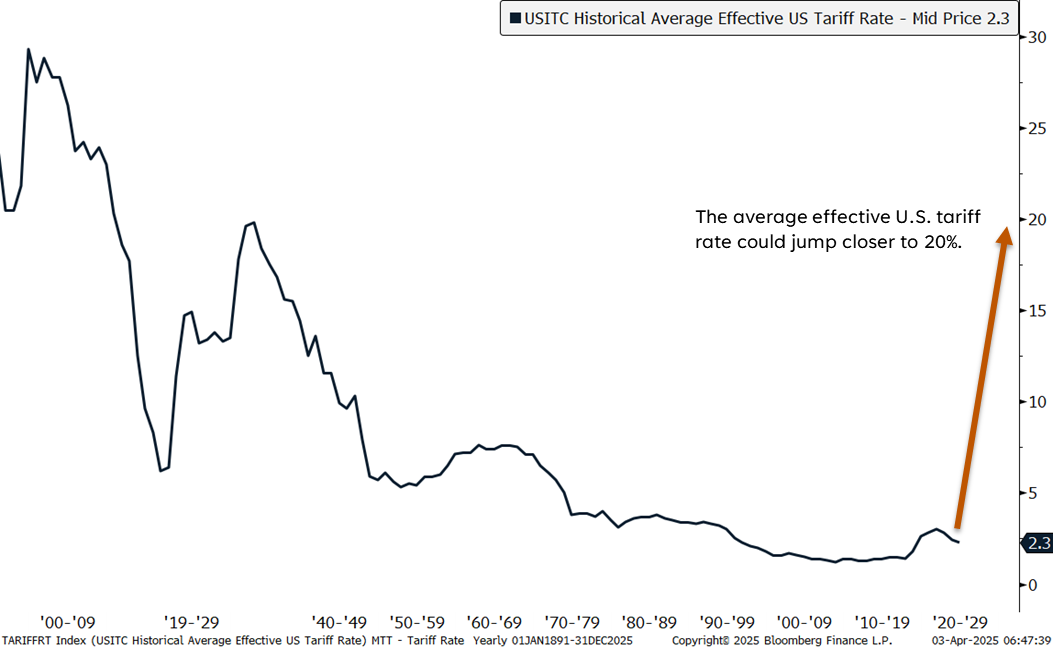

Average Tariff Rate: A Sharp Rise Ahead

The current state of affairs indicates that the weighted average U.S. tariff rate could surge from 2.3% in 2024 to a remarkable 20%, depending on various forecasts and sectoral tariffs that have yet to be announced. This drastic increase far surpasses market expectations, which had anticipated an effective tariff rate closer to 10–15%. Treasury Secretary Scott Bessent provided some context, cautioning trading partners that further escalation would inevitably lead to retaliation. -

Growth and Inflation: The Unwelcome Burden

A higher tariff rate introduces several unwelcome realities for the economy and markets. Investors can expect lower growth estimates along with added upside risk to inflation. Strategists are already revising their numbers downward following yesterday’s news, particularly in industries directly impacted by tariffs such as autos, air freight, logistics, food products, household goods, and construction materials. Some estimates suggest that S&P 500 earnings could face a reduction of 5-7% based on a 20% effective tariff rate assumption.

Regarding inflation, Goldman Sachs notes that every one percentage point increase in the tariff rate corresponds to a 0.1% rise in the core Personal Consumption Expenditures (PCE) Index – the preferred gauge used by the Federal Reserve (Fed). Utilizing this correlation and assuming an average tariff rate of 20%, they estimate that tariffs could add as much as 1.8% to core inflation this year.

Tariffs: A Mixed Bag for Global Trading Partners

All countries exporting goods to the United States are subject to a 10% tariff effective April 5th, with additional reciprocal tariffs proposed on around 60 other nations based on their tax rates on U.S imports. The European Union and Japan, both major trading partners of the US, are now subject to reciprocal tariff rates of 20% and 24%, respectively.

A notable exception from the universal 10% tariffs is Canada and Mexico, which were not included in the reciprocal tariff list. However, they still face a previously announced 25% tariff on non-United States-Mexico-Canada Agreement (USMCA) goods. In contrast, China was hit with an additional 34% tariff rate, bringing its total tariff rate to 54%. China also lost its de minimis exemption, meaning all imported goods from the country will face applicable duties, regardless of their value.

Tariff Exemptions and Silver Linings

Certain products have been excluded from the tariffs due to special circumstances. These include steel, aluminum, autos/auto parts, and materials like copper, pharmaceuticals, semiconductors, and lumber. The administration has also provided exemptions for gold, energy, and other select minerals that are not readily available in the United States.

The administration’s approach may be seen as an opening gambit aimed at gaining leverage rather than seeking actual implementation of such high rates. Moreover, investors can find silver linings in yesterday’s development. Not only have markets likely reached peak policy uncertainty, but increased revenues from tariffs could provide a significant boost to the fiscus. Strategic analysts argue that investors might take advantage of lower market prices to step back into stocks once confidence is restored.

Investors and lawmakers are likely to reevaluate existing political priorities in light of this trade development. Given the reduced growth expectations and higher revenue, added pressure will be placed on Congress to pass a tax bill which could include lower corporate and income tax rates. Furthermore, increased budget revenues generated from tariffs may further narrow the nation’s ballooning deficit.

Conclusion: The Way Ahead

Given the shockwaves generated by yesterday’s tariff announcement, investors would do well to keep a watchful eye on the road ahead. Economic trends will adjust in response to increased trade friction and shifting global economic dynamics. Lower market expectations and higher revenues could set off chain reactions affecting lawmakers’ priorities. LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) suggests that markets may now have reached peak uncertainty, bringing some balance and clarity into the market dynamics. As with any high-stakes event, patience is key as traders navigate through current uncertainties in anticipation of fresh opportunities.

Within fixed income asset classes, the STAAC favors a neutral weight to core bonds but prefers Mortgage-Backed Securities (MBS) over Investment-Grade Corporates due to an attractive risk-reward profile at present. As for sector calls, while valuations remain elevated in 2024, LPL’s experts do forecast future increases: we have tracked ProPicks AI in the last twelve months as well.

The next few days will be crucial in shaping investor sentiment and potentially setting new trends on trade policies. It is essential to stay vigilant about adjustments in the trade landscape while focusing on fundamental research for informed investment strategies.